Construction Insurance Costs: What Builders Actually Pay and Why It Changes

Insurance rarely stays flat for long in construction. Two builders can run similar crews, bid similar work, and still come back from renewal with very different numbers. One gets terms that still fit the business. The other gets a premium jump that cuts into the margin before the next job even starts.

That gap usually results from the way the carrier reads the operation. A contractor moving from light residential work into larger commercial construction is bringing a different level of exposure into the market, even if the company name and broker stay the same.

This guide looks at construction insurance costs from the builder’s side. The goal is to set realistic expectations, explain what moves premiums up, and show where contractors quietly lose money without noticing it soon enough.

Table of Contents

- What Does Construction Insurance Actually Cost?

- Why Construction Insurance Costs Vary So Much

- Cost Breakdown by Insurance Type

- Where Builders Overpay And Don’t Realize It

What Does Construction Insurance Actually Cost? (Baseline Ranges)

The safest way to talk about insurance costs is to treat every figure as a working band, not a promise. Pricing shifts with trade classification, payroll, state rules, claims history, deductibles, limits, and project type.

These bands help with early budgeting. They do not tell you what your business will pay after a bad claims year, a fleet expansion, a jump in payroll, or a move into heavier work. Construction insurance prices the operation you bring to market, not the one you think you still are.

Why Construction Insurance Costs Vary So Much

Insurance pricing in construction moves because exposure moves. Carriers are not only looking at the company in abstract terms. They are looking at the kind of work, the size of the jobs, the people doing the work, the history of losses, and the legal environment around the business.

Type of Work You Do

Trade classification is one of the first pricing filters. Home builders usually bring a different risk profile from commercial contractors.

Specialty trades vary even more. Roofing, excavation, demolition, and structural work tend to draw heavier scrutiny because one bad incident can get expensive very quickly.

This is where contractors often feel the pricing gap. From the builder’s point of view, the work may be familiar and well managed. From the carrier’s point of view, the real question is claim severity.

- How much damage can one failure cause?

- How big can one injury claim become?

- How exposed is the job to third-party loss?

Project Size and Contract Value

Larger jobs usually mean broader exposure. There is more value on site, more moving parts, more subcontracted work, more schedule pressure, and more contractual oversight. Such conditions affect insurance costs even before owner-specific requirements enter the picture.

Builder’s risk insurance makes this easy to see because it connects directly to the value under construction. Once project value grows, the insured value rises with it. GC contracts can push the cost higher through required limits, lien waivers, umbrella expectations, and project-specific endorsements..

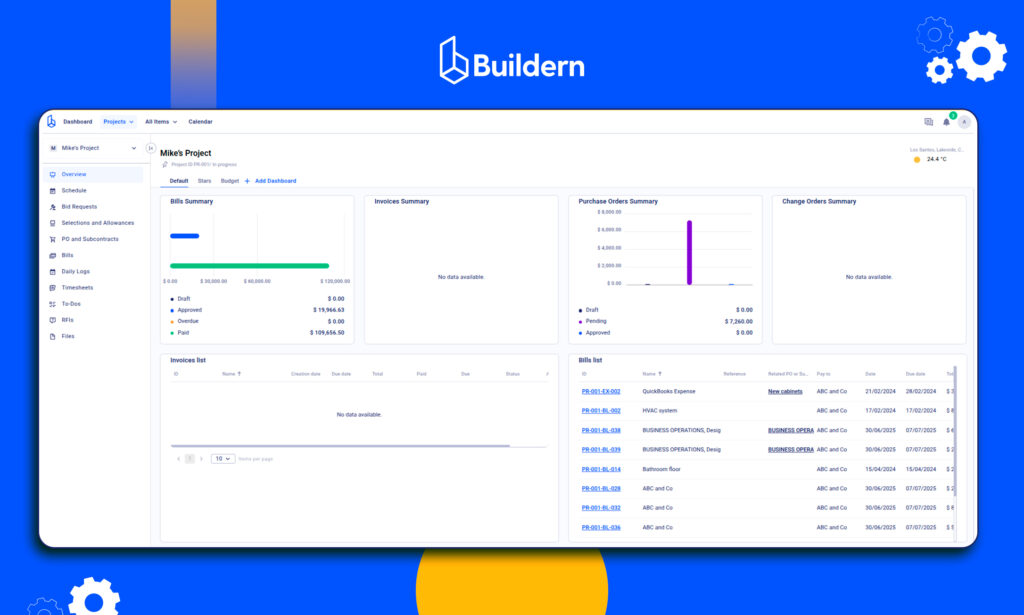

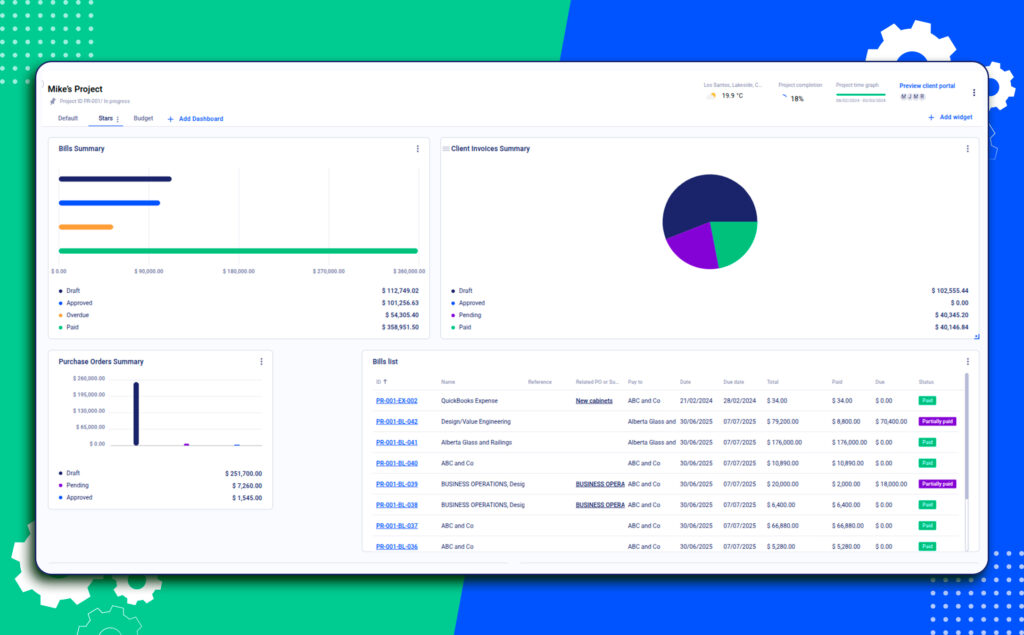

This is also where it helps to track project costs alongside insurance-related expenses. When those numbers are recorded in separate systems, it gets harder to see whether the insurance burden on a job still matches the way the project was originally priced.

Payroll and Labor Mix

Workers’ compensation is built around payroll and classification. That means growth in field payroll usually brings growth in premium. The structure of that payroll matters too. A company carrying a larger in-house workforce presents a different workers’ comp profile from one that leans more heavily on subcontractors.

Once subcontractor documentation slips, or the coverage on file is weak or outdated, exposure can move back up the chain. This is why managing subcontractor documentation and compliance through a dedicated portal has financial value. It affects who ends up carrying the risk.

Location and Regulations

Insurance is shaped heavily by state law, local claim trends, and the litigation environment. Workers’ comp is the clearest example because pricing rules and class-code treatment vary by state. Auto and liability lines also respond to regional claim severity, legal climate, and catastrophe exposure.

Therefore, contractors in different states can see very different pricing for work that looks similar on paper. The business may not have changed much, yet the market around it has.

Cost Breakdown by Insurance Type

When builders look at premium, they often see one number on the renewal package. Underwriters see a group of exposures. The premium reflects the insurer’s view of those exposures, not a generic charge for being in business.

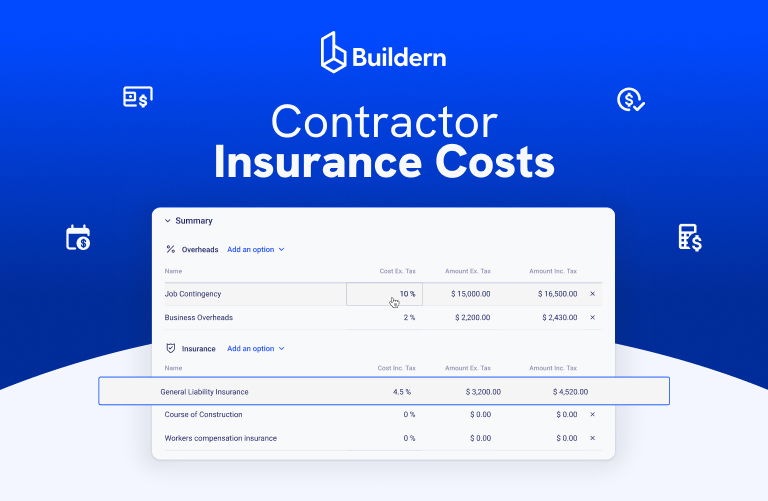

General Liability Insurance

General liability covers third-party bodily injury, property damage, and some personal and advertising injury claims. This is the line most owners and upstream parties expect to see first. Cost depends heavily on trade, revenue, project profile, subcontracting structure, and prior claims.

A contractor doing lower-hazard work may keep this line in a manageable range. However, a contractor in roofing or heavier specialty work may see a much higher number even before umbrella coverage is added.

General liability pricing follows the kind of damage the carrier thinks your operation can cause. Recent tendencies continue to show a wide liability range rather than one reliable “average” for construction.

Workers’ Compensation

Workers’ comp often gets misunderstood because contractors want one annual figure, while the actual price is built from payroll, class code, and experience. More payroll generally means more premium. Changes in labor mix can move the number again, while losses can keep pushing it in the wrong direction over time.

This line needs attention throughout the year. Payroll drift, overtime, inaccurate class assignments, and weak audit preparation can all change the final cost. Waiting until renewal to look at it usually means you are reacting after the number has already moved.

Practically speaking, payroll accuracy and class-code assignment materially affect final workers’ comp cost.

Builder’s Risk Insurance

Builder’s risk covers property under construction, subject to the terms of the policy. Cost depends on project value, location, frame type, catastrophe exposure, stored materials, project duration, and optional coverages such as soft costs.

The 1% to 5% budgeting band is useful as a first pass. It is still only a first pass. A coastal project with higher weather exposure and long duration will not price like a simpler inland build with a shorter timeline and fewer loss triggers.

Professional Liability (if applicable)

Professional liability matters where the contractor carries design responsibility, gives advice that creates professional exposure, or works in design-build and similar delivery models. It is not universal across every builder, but on the right jobs it becomes relevant quickly.

The cost depends on the type of service, the contract structure, prior claims, and how much professional responsibility is expected from the insured party.

💡For instance, Insureon currently reports annual professional liability ranges from roughly $400 to over $7,000 across small businesses.

Commercial Auto

Commercial auto remains one of the more difficult lines in the market.

Everything starting from repair costs, driver history, and up to trailer exposure matters. Even modest changes in fleet profile can move pricing more than contractors expect.

A light-duty pickup or van may still sit in a familiar annual range. Add heavier vehicles, more drivers, wider travel radius, or a rough claims record, and the number can move quickly.

Current market studies still describe auto as one of the more pressured lines, with monthly costs around the low hundreds for many small business accounts but a very wide annual spread overall.

Where Builders Overpay And Don’t Realize It

The moment your business changes and the paperwork stays put, the premium starts reflecting problems the company did not mean to buy.

- Overlapping or redundant coverage: Some builders carry policy features that respond to similar exposures or keep layers that no longer match the way the business actually operates.

- Misclassified risk: Wrong class codes or payroll treatment can inflate workers’ comp and liability pricing fast.

- Poor subcontractor documentation: A GC may end up carrying exposure that should sit with the subcontractor when the file is incomplete or the coverage on record does not hold up.

- Static policies while the business scales. Growth changes payroll, fleet count, project values, and contract requirements. When the insurance structure stays frozen, inefficiency usually follows.

When this or other issues arise, keeping financial visibility across jobs becomes a priority. Premium pressure rarely comes from one isolated place. More often it builds across payroll growth, fleet changes, claim activity, and project mix, then shows up in renewal pricing after the pattern is already established.

Therefore, having all the records and reports in a single database can make the picture clearer and job management less stressful.

To Sum Up…

Construction insurance costs move because the underlying business keeps moving. Payroll shifts. Fleet exposure grows. Project values rise. Contract language gets heavier. Once those changes are ignored for too long, renewal pricing usually becomes harder to control.

The practical takeaway is simple. Use ranges when budgeting. Keep classifications accurate before the audit. Make sure subcontractor files stay current. Treat claims as a financial event that touches margin, renewal pricing, and future flexibility. Insurance works better when it stays tied to the day-to-day reality of the business instead of coming up only when the policy is about to renew.

When Should a Builder Revisit the Insurance Structure Instead of Simply Renewing?

Usually, after a meaningful shift in project size, trade mix, payroll, fleet count, subcontracting strategy, or contract requirements. A company that waits for the renewal packet is usually looking at the problem later than it should.

Should a Small Contractor Carry Umbrella Coverage?

That depends on contract requirements, project type, fleet exposure, and the kind of third-party risk the business carries. Public work, larger commercial contracts, and broader liability requirements can push umbrella coverage into the picture earlier than many contractors expect.