Contractor Bonds vs Insurance: What Builders Actually Need to Protect Their Projects

Many builders carry strong insurance, clear certificates, and a thick subcontract file, then get blindsided when a trade falls apart and the job starts sliding. I have also seen teams feel comfortable because a bond was in place, then panic when they realized the surety was not there to absorb the contractor’s pain. That misunderstanding shows up all the time in construction project management, and it usually surfaces after the schedule is already under pressure.

The problems start early because contractor bonds vs insurance confusion often show up in the same contract package. They get reviewed at the same time, filed in the same folder, and treated as part of the same risk conversation.

On an active project, though, they serve different purposes, create different obligations, and affect the builder in different ways. This guide breaks that down from the project side, where decisions touch contracts, cash flow, vendor compliance, and execution.

Table of Contents

- Contractor Bonds vs Insurance at a Glance

- Why Builders Confuse Bonds and Insurance (And Why It Costs Money)

- What Contractor Bonds Actually Do

- What Insurance Actually Covers in Construction

- Where Bonds and Insurance Appear in the Project Lifecycle

- Risk Gaps Builders Don’t See Until It’s Too Late

- Key Highlights on Contractor Bonds vs Insurance Comparison

Contractor Bonds vs Insurance at a Glance

A construction bond gives the obligee a remedy path when the bonded party fails to meet a covered obligation. Insurance responds to covered losses, injuries, damage, and liability events tied to the business or the project.

Our table gives the quick version. The real problem starts when teams stop there and assume the tools overlap more than they actually do.

Why Builders Confuse Bonds and Insurance (And Why It Costs Money)

Most builders do not confuse these because they are careless. They confuse them because contracts bundle them together, brokers may discuss them in the same meeting, and project teams are already juggling scope, schedule, pricing, and compliance.

The mistake feels small at first. Yet, it gets expensive when a project starts moving off plan.

Same Requirement, Different Intent

Owners ask for bonding because they want protection tied to performance and payment obligations. Insurance requirements come from a different need. They are there to deal with covered incidents, property damage, injuries, and liability exposure tied to the work.

That distinction matters in preconstruction and matters even more after award. A builder who treats both tools like generic protection ends up reading the project through the wrong risk lens.

Misaligned Expectations in Contracts

This gets worse when GC contracts are drafted in a way that makes everything sound equally covered. A project manager may think the paperwork is complete because the policy limits are in place and the bond form has been submitted. An owner may assume a performance problem will unfold like an insurance claim. A subcontractor may believe payment protection exists because “the job is bonded,” even though the structure and claim rights say something more specific.

Bad assumptions travel fast in construction. Once they get embedded in the team’s thinking, they shape procurement decisions, subcontract language, and how people react when a job starts drifting.

Real-World Consequence

When builders misread contractor bonds vs insurance, the impact is rarely limited to paperwork. It usually shows up in a few practical ways:

- Time gets lost while teams figure out who is actually responsible

- Margins get squeezed as delays and mistakes pile up

- Negotiating weakens once disputes start to harden

- Overall project control slips on jobs that were already under pressure

What Contractor Bonds Actually Do

Construction bonds exist to support trust in a contract. They help an obligee move forward with the understanding that a surety stands behind a defined obligation.

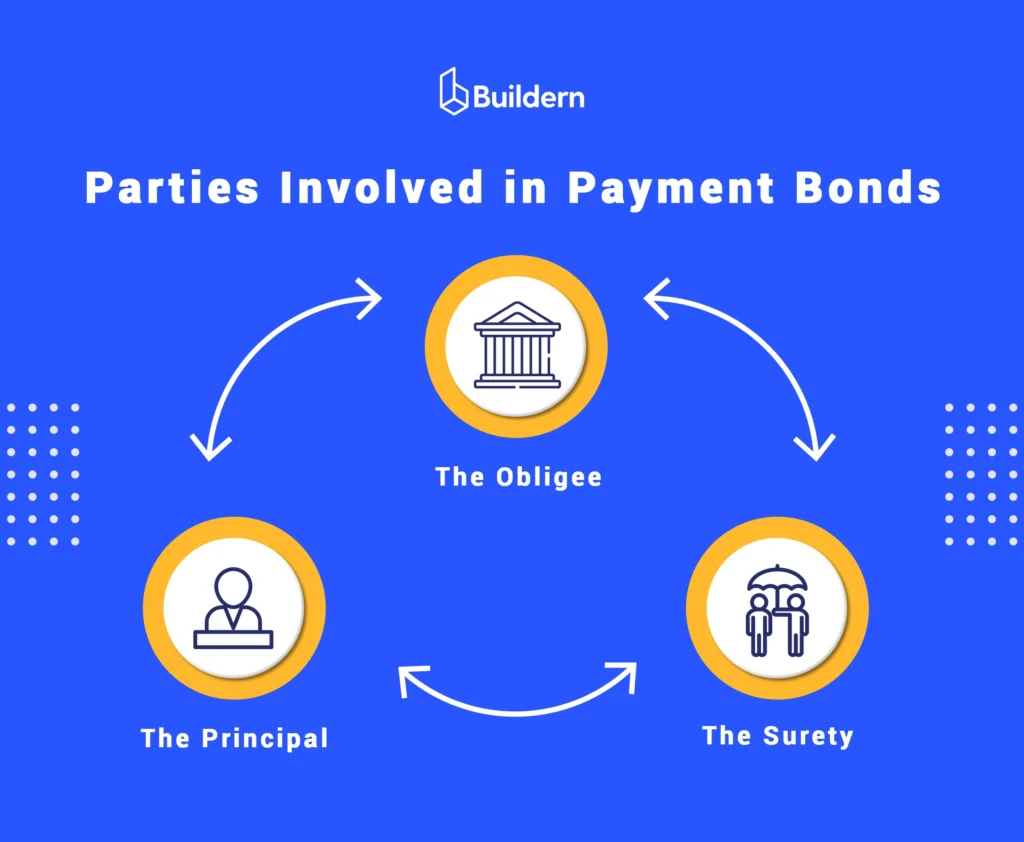

The Three-Party Structure (Principal, Obligee, Surety)

Every bond starts with three parties.

- The principal takes on the obligation.

- The obligee requires the bond and receives the protection built into it.

- The surety issues the bond after reviewing the principal’s financial strength, operating history, and capacity to perform.

That structure matters because it shapes the direction of protection. The surety is not functioning like a general insurer that simply absorbs project pain in exchange for premium. The contractor remains financially tied to the obligation. If the surety pays out or funds a response, indemnity usually follows.

Core Bond Types in Construction

A bid bond supports the tender process. It tells the owner that the bidder is serious, capable of entering the contract, and prepared to provide the required follow-on security if selected.

A performance bond comes into play when the contractor fails to carry the contract through in a way the bond and contract recognize as default. Depending on the terms and the facts, the surety may investigate, support completion, arrange replacement performance, or finance a path forward.

A payment bond addresses payment exposure lower in the chain. It helps protect certain subcontractors, suppliers, and labor claimants when the bonded contractor does not pay as required.

What Triggers a Bond Claim

Bond claims grow out of obligation failure. The most common examples are non-performance, serious contract breach, and non-payment to qualified downstream parties.

A contractor who cannot maintain performance, walks away from the work, or defaults under the contract can push the project into performance bond territory. A contractor who fails to pay subcontractors or suppliers can create payment bond exposure. The important point is that a bond claim usually starts with a breakdown in the contractual promise that the bond was written to support.

What Insurance Actually Covers in Construction

Insurance is part of the project’s day-to-day protection structure. It exists to respond when covered events happen during operations.

What Insurance Does Well

Insurance handles many of the events builders face across the life of a project. General liability can respond to third-party injury or property damage claims. Builder’s risk may respond to certain covered damage to the work in progress. Workers’ compensation deals with employee injury exposure under the applicable rules. Commercial auto, umbrella, professional liability, pollution, and other policies each cover their own slice of risk.

This is why insurance remains active throughout mobilization, active production, punch, and closeout. It is woven into the operating life of the project.

What It Does Not Cover

Insurance does not guarantee contract performance. It does not rescue an owner from a failed contractor simply because the schedule fell apart, does not turn a subcontractor default into a covered claim, and cannot erase the contractor’s financial responsibility under a bond.

Builders get hurt when they assume their insurance program reaches problems that are really commercial, operational, or contractual in nature.

Where Bonds and Insurance Appear in the Project Lifecycle

This is where builder decisions start getting sharper. Insurance stays relevant throughout the job. Bonds matter most when contract obligations are under real stress.

Preconstruction Phase

In preconstruction, bonding capacity affects what a contractor can pursue and how much backlog it can carry without overextending the business. Sureties look closely at working capital, net worth, internal controls, work history, project mix, and management discipline.

Insurance enters early as well through contract requirements, policy limits, endorsements, and subcontractor compliance review. The team has to know what coverage is required, who must carry it, and whether the project structure creates unusual exposure.

Active Construction Phase

During active construction, insurance touches daily project life. Project teams need current policies, accurate certificates, and visibility into subcontractor compliance because expired or missing coverage creates direct exposure.

Bonding becomes central when the project starts moving toward default territory. That usually shows up through missed obligations, sustained underperformance, unresolved non-payment, or a breakdown in the contractor’s ability to carry the work.

Closeout and Post-Completion

Closeout can still generate bond and insurance pressure.

- Payment disputes may remain unresolved.

- Punch work can stall.

- Documentation gaps can affect completion.

Insurance keeps running in the background because claims can surface after substantial completion. Completed operations exposure does not vanish when the trailer leaves.

Risk Gaps Builders Don’t See Until It’s Too Late

Some of the most expensive failures start with assumptions that feel normal in a busy office.

→ A builder may assume insurance will respond when a subcontractor falls apart operationally. Standard project insurance does not exist for that problem.

→ A contractor may feel reassured by bonding and forget that the surety expects the principal to stand behind the loss. That misunderstanding can turn a stressful project into a liquidity problem.

→ A company may also treat bonding and insurance as compliance paperwork only. When the documents are disconnected from budgets, commitments, and live project status, the team loses the ability to see risk forming before it turns into a formal dispute.

- Insurance does not fix subcontractor failure.

- Bond loss still lands back on the contractor through indemnity in many cases.

- Scattered documentation hides exposure.

- A project team cannot manage what it cannot see in one place.

Key Highlights on Contractor Bonds vs Insurance Comparison

Builders need both bonds and insurance on the right jobs, but they need them for different reasons. The danger starts when those reasons get blurred. Strong project control comes from understanding where each tool fits, reading the contract correctly, and keeping compliance tied to live execution.

- Bond claims come out of broken contractual obligations.

- Insurance claims come out of covered incidents, losses, and liability events.

- Bonding capacity shapes how much work a builder can take on safely.

- Better visibility across contracts, finances, and project status cuts down avoidable exposure.

Are Bonds a Type of Insurance?

No. Bonds are issued by sureties and support a defined contractual obligation owed to the obligee. Insurance is built around covered loss events and liability exposure affecting the insured party.

What Is the Difference Between a Bond and Insurance?

A bond gives the obligee recourse when the contractor fails to meet a covered obligation. Insurance gives the contractor or business protection when a covered claim, accident, damage event, or loss takes place under the policy terms.

How Do Bonding Limits Affect My Backlog?

Bonding limits influence how much work a builder can carry because sureties review financial capacity, current workload, internal controls, and past performance.

A contractor can run into trouble long before cash runs out if backlog grows faster than management capacity and surety support. That is why builders need current visibility into commitments, budgets, progress, and vendor risk across the entire pipeline.