Mastering the AIA G703 Continuation Sheet: The Ultimate Guide to the Schedule of Values

Construction invoicing is all about translating field progress and contract value into defensible, review-ready financial documentation. When that translation fails, certification slows, margins blur, and cash flow becomes unpredictable.

The AIA Document G703 is where that translation happens. While the AIA G702 summarizes the amount due, the G703 is where the contractor proves the math. Every scheduled value, percentage complete, retainage calculation, and cumulative total lives here. If the numbers do not reconcile at this level, approval will not move forward.

To help you avoid the cumulative effect of errors through billing cycles, I’ve decided to focus mainly on the technical side of the Schedule of Values: structure, reconciliation logic, retainage modeling, audit controls, and defensibility.

My goal here is simple. Help you build a G703 that stands up to architect review, lender scrutiny, and financial audit without revision.

Table of Contents

- What Is AIA G703 and Why It Matters More Than You Think

- The Anatomy of the AIA G703 Columns (Line-by-Line Technical Breakdown)

- Building a Defensible Schedule of Values

- Integrating Change Orders Without Breaking the Math

- Retainage Modeling on the G703

- 4 Common AIA G703 Errors That Delay Certification

- Digital vs Spreadsheet-Based AIA G703 Workflows

What Is AIA G703 and Why It Matters More Than You Think

The AIA Document G703 is the detailed construction Schedule of Values attached to each pay application. It itemizes the contract into measurable components and tracks financial progress line by line. While it may appear to be a supporting worksheet, it functions as the mathematical backbone of AIA billing.

Every billing cycle builds on the previous one. The G703 accumulates:

- Original scheduled values

- Approved change order adjustments

- Work completed to date

- Stored materials

- Retainage withheld

- Balance remaining

Because it carries cumulative history, even minor miscalculations compound over time. A rounding inconsistency in month two becomes a reconciliation problem in month six. By the time substantial completion approaches, unresolved math discrepancies can distort retainage release and final payment calculations.

For architects, owners, lenders, and auditors, the G703 is where financial transparency is tested. If percentages exceed realistic progress, if balances go negative, or if totals fail to reconcile with the contract sum, the review process slows immediately.

The form does not simply report progress. It defines the financial structure of the project in motion.

The Relationship Between G703 and G702

The AIA Document G702 is the summary and certification page. It presents the total amount due for the current billing period.

The G703 is the detailed proof behind that summary.

Every number on the G702 must trace directly to the continuation sheet. The adjusted contract sum, total completed to date, retainage, and balance to finish are all derived from the G703 calculations. If the totals do not reconcile precisely, certification under the G702 is at risk.

In practical terms, the G702 asks for payment, while the G703 justifies it.

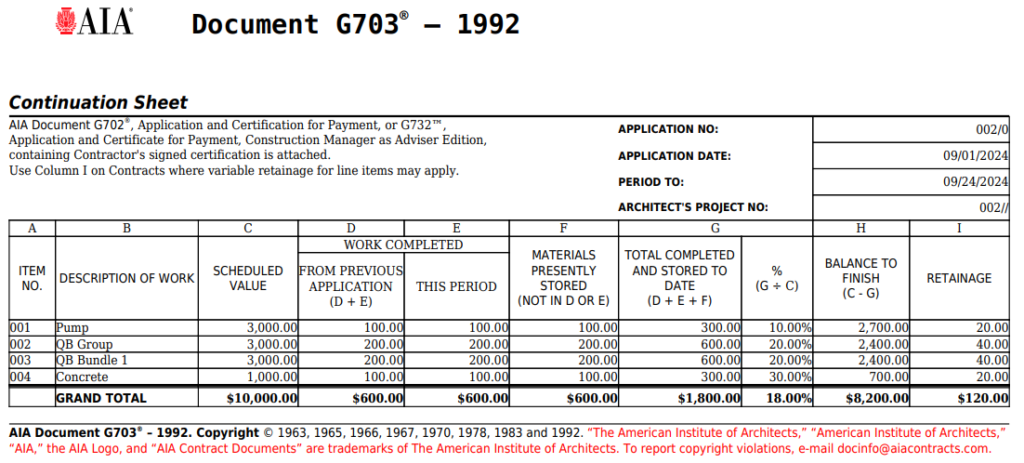

The Anatomy of the AIA G703 Columns (Line-by-Line Technical Breakdown)

The AIA Document G703 follows a structured column format. The layout is simple; however, the control logic behind it is not. Each column affects cumulative totals and certification under the AIA Document G702.

Below is the technical function of each major column and where errors typically occur.

Scheduled Value (Column B)

This is the contract baseline for each line item. It must reflect the original Schedule of Values plus any approved change orders affecting that specific scope.

If Column B totals do not equal the adjusted contract sum, the application fails immediately. Avoid modifying scheduled values outside of formally executed changes.

Work Completed This Period (Column C)

This column captures the dollar value of work performed during the current billing cycle.

The most common issue is percentage-based estimation that does not align with actual progress. Overstating progress here creates cumulative distortions in later periods.

Materials Stored (Column D)

This reflects approved materials purchased but not yet installed.

Stored materials must be supported by documentation and cannot exceed the scheduled value of the line item. Failing to separate installed work from stored materials creates review friction.

Total Completed and Stored to Date (Column E)

This is the cumulative total: prior billing plus current period work and stored materials.

Formula logic must hold:

Current cumulative = previous cumulative + current period

If this column does not reconcile with prior applications, the discrepancy compounds forward.

Percentage Complete (Column F)

This is derived, not estimated independently. It equals cumulative completed to date divided by the scheduled value.

Manual rounding is a common trap. Even small rounding differences can produce visible inconsistencies across large projects.

Balance to Finish (Column G)

This represents the remaining value on the line item:

Scheduled value minus total completed to date

Negative balances indicate overbilling or incorrect cumulative math. Architects flag these instantly.

Retainage (Column H or Retainage Fields)

Retainage is typically calculated as a percentage of completed work. It must align with contract terms and match the summary shown on the G702.

Incorrect retainage allocation by line item leads to mismatched totals and delayed certification.

The structure of the G703 is linear, with every column depending on the integrity of the previous one. Precision at this level determines whether the payment application withstands review without revision.

Building a Defensible Schedule of Values

A strong AIA Document G703 begins long before the first pay application is submitted. The quality of the Schedule of Values determines how smoothly billing, certification, and cost control will function throughout the project.

For accountants and estimators, the SOV is not just a billing format. It is a financial structure that must withstand architect review, lender scrutiny, and internal audit. A defensible SOV is transparent, balanced, and aligned with how the project is actually managed.

Translating the Estimate Into the SOV

The most reliable Schedule of Values originates directly from the approved estimate. Each major construction cost code or work package should map logically into a billing line item.

Problems arise when the SOV is reconstructed manually or simplified excessively for billing. If the SOV does not reflect how costs were estimated and budgeted, reconciliation becomes difficult. Margin tracking weakens, and percentage-complete calculations lose credibility.

The objective here is alignment. The estimate establishes financial intent. The SOV operationalizes it for billing.

Proper Level of Granularity

Granularity determines transparency.

If line items are too broad, percentage complete becomes subjective and difficult to defend. A single “General Conditions” or “Interior Build-Out” line may obscure meaningful progress distinctions.

If line items are too fragmented, administration becomes inefficient. Excessive detail increases reconciliation complexity and invites minor rounding inconsistencies.

The defensible position sits between those extremes. Line items should reflect measurable scopes of work that correspond to trade divisions or logical construction phases. The structure must allow accurate progress tracking without creating unnecessary billing noise.

Avoiding Front-Loading Accusations

Front-loading occurs when disproportionate value is assigned to early-stage work to accelerate cash flow. Architects and lenders review early billing cycles carefully for this reason.

An SOV that heavily weights mobilization, site preparation, or preliminary items relative to total project value invites scrutiny. Even if mathematically defensible, perception alone can slow certification.

Balanced allocation reduces that risk. Scheduled values should reflect realistic labor, material, and sequencing distribution. When early trades are billed at percentages that align with visible progress, approval proceeds more predictably.

Aligning SOV With Cost Control Systems

The Schedule of Values should not exist separately from accounting and project management systems. When the SOV is disconnected from internal cost tracking, inconsistencies emerge between billed revenue and incurred costs.

Alignment requires that:

- Cost codes correspond to SOV line items.

- Approved change orders update both contract value and internal budgets.

- Cumulative billing history is traceable to cost reports.

Modern AIA-style billing workflows support this integration by syncing estimating, change management, and pay application tracking in one structured environment. When billing data flows from live project controls rather than isolated spreadsheets, the SOV remains consistent across financial reporting and invoicing.

A defensible Schedule of Values is therefore not just well formatted. It is structurally integrated into the project’s financial management systems.

Integrating Change Orders Without Breaking the Math

Change orders are where many AIA Document G703 structures begin to lose integrity. Each approved modification increases or decreases the contract sum, and that adjustment must be reflected precisely in the Scheduled Value totals. If handled informally or added inconsistently, cumulative discrepancies appear in later billing cycles.

Only fully executed change orders should adjust the Schedule of Values. Pending or disputed amounts may be tracked internally, but they should not alter the official contract baseline used for billing. Inflating the Scheduled Value column before formal approval exposes the application to reduction during review and creates reconciliation risk.

When a change order is approved, the adjustment must flow cleanly into the affected line item and into the overall contract total. The sum of all Scheduled Values must always equal the adjusted contract value. That tie-out is non-negotiable. If the total of the continuation sheet does not reconcile to the revised contract sum, certification under the AIA Document G702 will be delayed immediately.

Every modification also requires cumulative verification. Previously billed amounts must remain accurate, percentages must be recalculated correctly, and no portion of the added scope should be billed twice.

Construction change orders have the power to reset the mathematical baseline.

Maintaining discipline at this step protects the integrity of every future payment application.

Retainage Modeling on the G703 AIA Billing

Retainage on the AIA Document G703 is a cumulative financial control that affects cash flow, balance-to-finish calculations, and final payment accuracy. When modeled incorrectly at the line-item level, discrepancies surface quickly during review.

Retainage must reflect the exact terms of the contract and be applied consistently across billing cycles. Variations in application often occur when stored materials, partial releases, or trade-specific agreements are involved.

Common control points include:

- Applying the correct retainage percentage to completed work versus stored materials.

- Adjusting retainage properly after substantial completion or partial release approvals.

- Ensuring cumulative retainage withheld ties precisely to the summary shown on the AIA Document G702.

- Verifying that balance-to-finish calculations account for retainage without distorting remaining contract value.

Because retainage is cumulative, small miscalculations compound over time. Accurate modeling ensures that release at project closeout proceeds without reconciliation disputes or delayed final payment.

4 Common AIA G703 Errors That Delay Certification

Even when the overall GC contract total appears correct, certification often stalls because of structural issues within the AIA G703. Architects and reviewers focus on internal consistency. When line-item math signals risk, the application is reduced or returned for clarification.

Below are the most frequent technical errors shared by fellow accountants that trigger delays.

Overbilling Individual Line Items

Overbilling occurs when the percentage completed for a specific line item exceeds realistic physical progress. Even if the total contract value remains intact, disproportionate billing on one trade signals front-loading or estimation error.

Reviewers compare progress to observable site conditions. If billed progress cannot be substantiated, certification may be reduced to a defensible amount.

Negative Balance to Finish

A negative balance to finish indicates that cumulative billed amounts exceed the scheduled value for that line item. This typically results from rounding errors, misapplied change orders, or incorrect cumulative calculations.

Negative balances are immediate red flags. They suggest structural math failure and must be corrected before approval.

Stored Materials Exceeding Line Item Value

Stored materials should never exceed the total scheduled value allocated to that scope. When Column D pushes cumulative totals beyond the contract allocation for a line item, it creates an overbilling condition.

Proper construction documentation and careful allocation are essential to prevent this distortion.

Retainage Inconsistency

Retainage must be applied consistently at the line-item level and reconcile exactly with the summary shown on the AIA Document G702. Mismatched percentages, partial releases applied incorrectly, or manual overrides often cause unnecessary issues.

Because retainage affects totals and balance-to-finish values, inconsistency in this column delays certification until corrected.

In each case, the issue is not complexity but precision. The G703 in AIA billing must remain internally coherent across all columns for certification to proceed without revision.

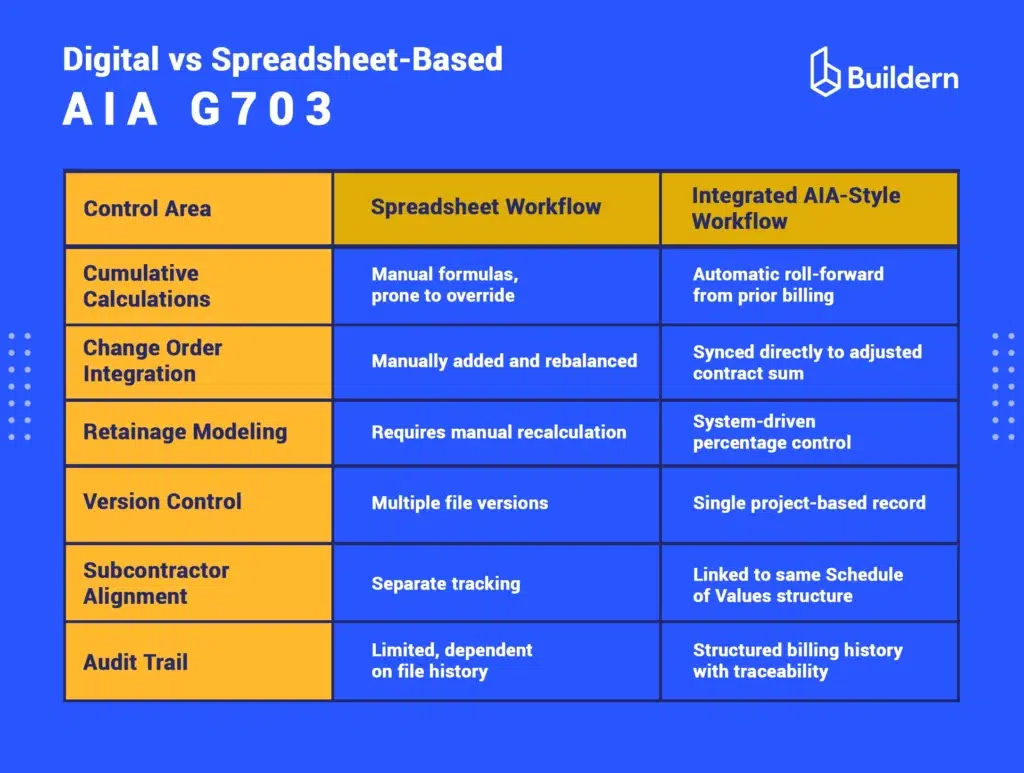

Digital vs Spreadsheet-Based AIA G703 Workflows

Many teams still manage the AIA Document G703 in standalone spreadsheets. While flexible, spreadsheet-based workflows introduce structural risk because the math depends on manual control rather than system logic.

Common weaknesses include:

- Formulas that can be edited or overwritten unintentionally

- Cumulative totals are dependent on strict version tracking

- Change order adjustments requiring manual redistribution

- Retainage recalculations handled outside a controlled structure

Individually, these issues seem minor. Across multiple billing cycles, they compound.

The deeper concern is fragmentation. Estimating exists in one file, cost tracking in another, and change orders in separate logs.

Integrated AIA-style billing workflows reduce that exposure by connecting the Schedule of Values directly to approved COs.

As a result, the cumulative math updates automatically. The adjusted contract sum remains aligned with executed modifications. The continuation sheet becomes part of the project’s financial control system rather than a parallel spreadsheet exercise.

Benefits of Integrated AIA-Style Billing Systems

Integrated AIA-style billing systems are designed to mirror the logic of both the AIA Document G703 and the AIA Document G702 within a connected financial environment.

Instead of reconstructing the Schedule of Values each month, the system maintains a live contract baseline that evolves with approved changes and prior billings.

Key operational advantages include:

- Automatic cumulative calculations that roll forward accurately from prior periods

- Real-time change order syncing to the adjusted contract sum

- Consistent retainage recalculation aligned with contract terms

- Subcontractor pay application alignment with the same SOV structure

- Centralized audit trail preserving billing history and revisions

To sum up, my suggestion is to treat AIA G703 as the mathematical backbone of the entire AIA billing process. When structured correctly, aligned with the estimate, integrated with change orders, and reconciled each cycle cumulatively, it becomes a stable financial record rather than a recurring risk point.

Use integrated digital solutions to enhance your financial performance and bring clarity to the organizational environment.

How Does the AIA G703 Affect Final Payment?

Final payment depends on accurate cumulative tracking throughout the project. Errors that persist across billing cycles often surface during retainage release and closeout reconciliation.

Should Subcontractor Pay Applications Mirror the Prime Contractor’s SOV Structure?

Alignment is recommended. When subcontractor billing follows the same structural logic as the prime Schedule of Values, reconciliation becomes more predictable and defensible.

How Granular Should a Schedule of Values Be?

Granularity should reflect measurable scopes of work, typically aligned with trade divisions or cost codes. Too broad reduces transparency. Too much detail increases administrative burden and rounding risk.