Percentage of Completion Method Explained for Builders

I have never liked financial reports that tell the truth too late.

Construction projects run for months, sometimes years. If revenue were recorded only when the job finishes, the numbers in between would be distorted. One quarter would look weak, the next would look inflated, and neither would reflect what was actually happening on the project.

That is why construction accounting uses the percentage of completion method. It recognizes revenue and expenses gradually as work progresses, instead of waiting until the very end. In practice, that gives builders a clearer view of performance while the job is still active, which makes better decisions possible before problems harden into losses.

Table of Contents

- What Is the Percentage of Completion Method in Construction

- Why Construction Companies Use the Percentage of Completion Method

- How to Calculate Percentage of Completion

- Example of the Percentage of Completion Method

- The Role of Work in Progress (WIP) Reports

- Percentage of Completion vs Completed Contract Method

What Is the Percentage of Completion Method in Construction

The percentage of completion method is a way of recognizing revenue over time rather than all at once. Under current U.S. GAAP, ASC 606 establishes a revenue recognition framework, and under international standards, IFRS 15 does the same. Both standards support recognizing revenue over time when the contract meets the relevant criteria, rather than only at final completion.

In builder terms, the concept is simple:

- Revenue is recognized gradually

- Revenue recognition is tied to project progress

- It is commonly used on long-term contracts

- It helps show project profitability while work is still underway

That last point matters most.

Construction revenue recognition should match the actual pace of execution. If the project is 25% complete, the accounting should reflect roughly that level of earned revenue, assuming the measurement method is sound.

This is why the method is so common in construction. Most builders do not run short-term, one-day contracts. They run jobs that span phases, draw schedules, trade sequencing, procurement delays, and cost movement over time. The construction accounting has to keep up with that reality.

Another reason the method matters is that construction does not unfold evenly. Some months are heavy on procurement, while others are labor-intensive. Some phases move quickly, while others slow down because of inspections, weather, or client decisions. If accounting waits until the very end to recognize revenue, it hides the operational story of the job.

The percentage of completion method fixes that by keeping the financial picture closer to what the field is actually producing.

Why Construction Companies Use the Percentage of Completion Method

We do not use this method because it sounds sophisticated. In fact, the main reason is that the alternative often creates a weaker picture of what the business is doing.

Here are some other factors that work in favor of this method.

More Accurate Financial Reporting

If revenue were recorded only at the end of a long project, the financial statements in the middle of the job would look incomplete. Costs would be showing up, but the related revenue would not. That creates volatility that is not operationally useful.

The percentage of completion method smooths that distortion. It aligns revenue with actual progress, which makes the financial statements more representative of what the company has earned so far. That also helps owners, lenders, and internal leadership read performance more realistically across the year instead of reacting to artificial swings caused by timing alone.

Better Visibility Into Project Profitability

Now the method becomes practical, not theoretical.

When revenue is recognized gradually, builders can compare:

- Earned revenue

- Actual costs incurred

- Expected gross profit

That makes it easier to see whether a project is holding margin or slipping. If labor productivity is weaker than expected or material costs rise faster than planned, the impact starts to surface sooner.

Without that visibility, profitability analysis arrives late. By then, the job may already be carrying damage that cannot be recovered.

It also helps at the portfolio level. When several projects are active at the same time, construction management needs to know which jobs are performing and which ones are quietly deteriorating. If revenue is delayed until closeout, one strong completion can hide multiple active problems. Percentage of completion gives a more balanced view across the whole backlog.

Improved Cash Flow Planning

Cash flow is not the same thing as profit, but the two are closely related in construction. When revenue recognition tracks progress more realistically, management gets a cleaner view of:

- What has been earned

- What has been billed

- And what still needs to be collected

It also provides insights on how current performance affects future cash position, improving project planning around payables, payroll, procurement timing, and financing needs.

Moreover, the method gives finance and operations a better shared language. The accounting team can see where earned revenue stands. The project team can compare that against actual field progress and billings. Such alignment matters because construction cash flow problems often start when accounting and job performance drift apart without anyone noticing early.

Required for Many Long-Term Contracts

This is also a standards issue, not just an internal management choice.

- Under ASC 606, revenue is recognized in a way that reflects the transfer of promised goods or services to the customer.

- Under IFRS 15, revenue is recognized to depict that transfer in an amount reflecting the consideration expected.

IFRS 15 specifically requires revenue to be recognized over time when the relevant criteria are met and progress toward completion can be measured appropriately.

In practical construction terms, that means many long-duration contracts are not well represented by waiting until the very end to record all revenue. The accounting needs to follow the economics of the job.

How to Calculate Percentage of Completion

There are different ways to measure progress, but the most common method in construction is the cost-to-cost method.

The core idea is straightforward:

Once that percentage is known, it is applied to the contract value to determine how much revenue should be recognized to date.

Cost-to-Cost Method (Most Used in Construction)

This method is widely used because cost tends to be the cleanest measurable signal of progress on many jobs.

Conceptually, the steps are:

- Determine total estimated project cost

- Calculate actual costs incurred to date

- Divide actual costs by total estimated cost

- Use that percentage to determine earned revenue

- Subtract recognized costs from recognized revenue to determine gross profit to date

This works well when cost is a reliable indicator of progress. It becomes less useful if cost timing is distorted by unusual procurement patterns, large upfront deposits, or other non-linear job conditions. That is why the method still needs judgment.

Another practical point is that the total estimated cost cannot stay frozen if the job changes. If labor productivity drops, material pricing shifts, or a subcontractor scope increases, the forecasted final cost must be updated. Otherwise, the percentage complete calculation starts giving a false sense of accuracy. The method is only as reliable as the current job cost forecast behind it.

Example of the Percentage of Completion Method

Project details:

- Contract value: $2,000,000

- Estimated total cost: $1,600,000

- Costs incurred after 6 months: $400,000

1: Calculate percent complete

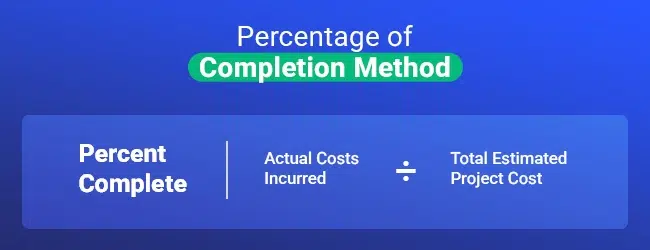

Percent complete = Actual costs incurred ÷ Total estimated project cost

$400,000 ÷ $1,600,000 = 25%

So the project is 25% complete from an accounting standpoint.

2: Calculate revenue recognized

Revenue recognized = Contract value × Percent complete

$2,000,000 × 25% = $500,000

That means the company should recognize $500,000 of revenue to date.

3: Calculate gross profit recognized

Gross profit = Revenue recognized − Costs incurred

$500,000 − $400,000 = $100,000

So the gross profit recognized so far is $100,000.

That example shows the logic clearly:

- The job is 25% complete

- 25% of the contract value is recognized as revenue

- Current gross profit can be measured before the project is finished

This is exactly why the percentage of completion accounting matters. It gives a clearer picture of performance while work is still in motion.

Six months into the job, the company already has a view of earned revenue and gross profit. That allows earlier questions about whether the project is tracking as expected or whether the original assumptions need to be revisited.

The Role of Work in Progress (WIP) Reports

A construction WIP report connects the accounting view of progress to the operational and billing reality of the job. It usually brings together four core elements:

- Percent complete

- Earned revenue

- Billings to date

- Overbilling or underbilling position

I believe the connection matters because recognized revenue and billed revenue are not the same thing. A project can be underbilled or overbilled. Neither condition is automatically good or bad. But both need to be visible.

A good WIP report helps answer questions like:

- Are we earning revenue faster than we are billing?

- Are we billing ahead of actual performance?

- Is a reported margin supported by the current project progress?

- Are there jobs where revenue recognition and billings are drifting apart?

Therefore, WIP reporting is so important in construction. It ties together the accounting method, the billing process, and the real status of the work.

It also helps expose jobs that look stable at first glance but are weakening underneath. A PM may feel the work is moving and finance may see that invoices are going out, but the WIP report can show that earned revenue is lagging, or that projected gross profit is narrowing faster than expected. That early signal is often the difference between making a correction and absorbing a loss later.

Percentage of Completion vs Completed Contract Method

The comparison usually comes down to timing and visibility.

It’s the basic distinction behind completed contract vs percentage of completion.

The completed contract method delays revenue recognition until the job is finished. It makes sense on short-duration work where the project is completed quickly and interim financial distortion is limited.

The percentage of completion method is generally more useful on long-term projects because it gives earlier visibility into project performance, margin movement, billing, and cost overruns.

Another way to think about it is this: the completed contract method tells the story at the end, while percentage of completion helps tell it during the job.

For builders managing active risk, earlier visibility is usually more useful than cleaner hindsight.

Final Thoughts

For builders, the method offers more than compliance. It improves visibility while the work is still active. That means stronger profitability tracking, better cash flow planning, and earlier detection of jobs that are drifting.

When the method is supported by disciplined cost forecasting and current WIP reporting, it becomes more than an accounting rule. It becomes part of how a builder keeps financial control while the project is still underway.

One of the biggest misconceptions about this method is that it belongs only to accounting. In reality, it works best when accounting, construction project management, and cost control stay connected.

The stronger that connection is, the more useful the method becomes for actual decision-making during the life of the job.